You file it yourself — we prepare everything · 49 states + DC

They broke the law.Make them pay you.

When a credit bureau or debt collector breaks the law, credit monitoring just watches and letter tools just ask. 28Solutio hands you the whole case — dispute to default judgment, court-ready — and you keep the statutory damages.

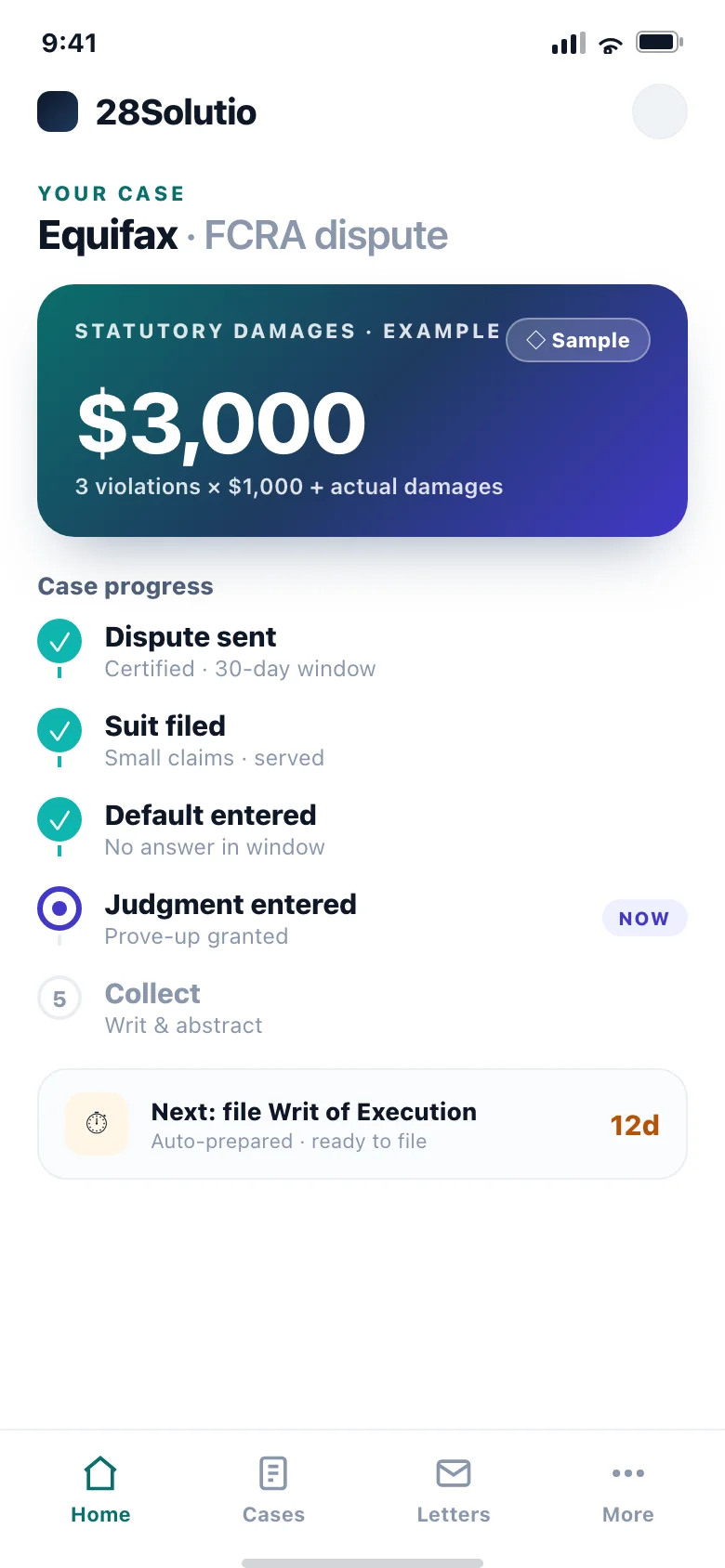

$3,000 example recovery · 3 × $1,000/violation

Built onFCRA §1681FDCPA §1692Bank-level encryptionUSPS certified49 states + DC

1Dispute2File3Win by default4Collect

What you can walk away with

Willful violations found:3

3 violations: $300 to $3,000 in statutory damages

statutory damages, recoverable

What you pay: $35/letter or $49/mo · Run your own numbers →

15 U.S.C. §1681n(a)(1)(A) · willful violations

Courts set the amount within the statutory range, and only for violations proved willful. Illustrative — not a prediction, promise, or legal advice.

+ actual damages

on top of that

the real losses they caused you

50

jurisdictions mapped

49 states + DC · CA & TX court-ready today

The whole case, in your pocket

Dispute, file, and collect —

from one app.

The FTC found more than 1 in 5 consumers had a verified error on a credit report — and under the FCRA, every one can be a violation worth $100–$1,000. 28Solutio finds them, cites the exact statute, and builds the paper trail that holds up in court.

Source: FTC · 2012 report to Congress (Section 319)

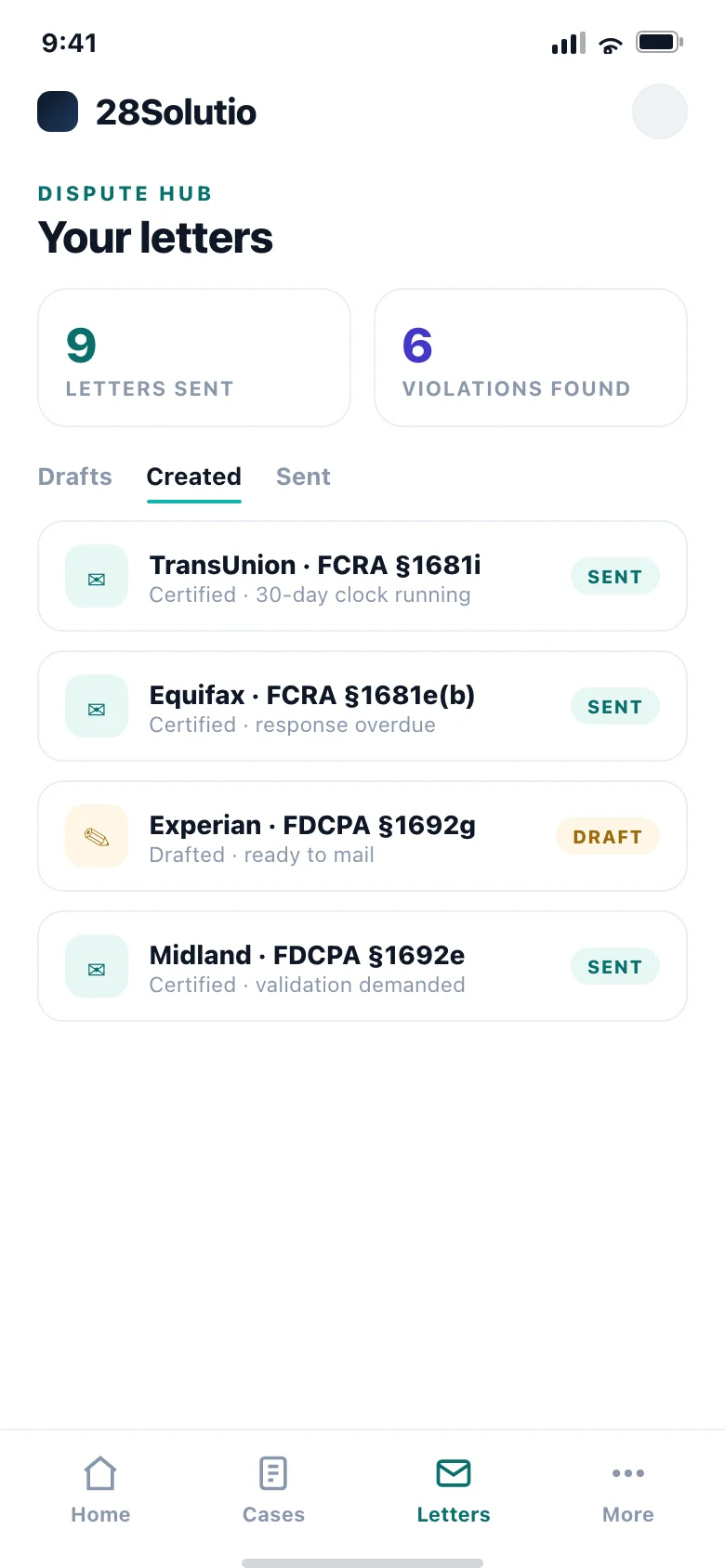

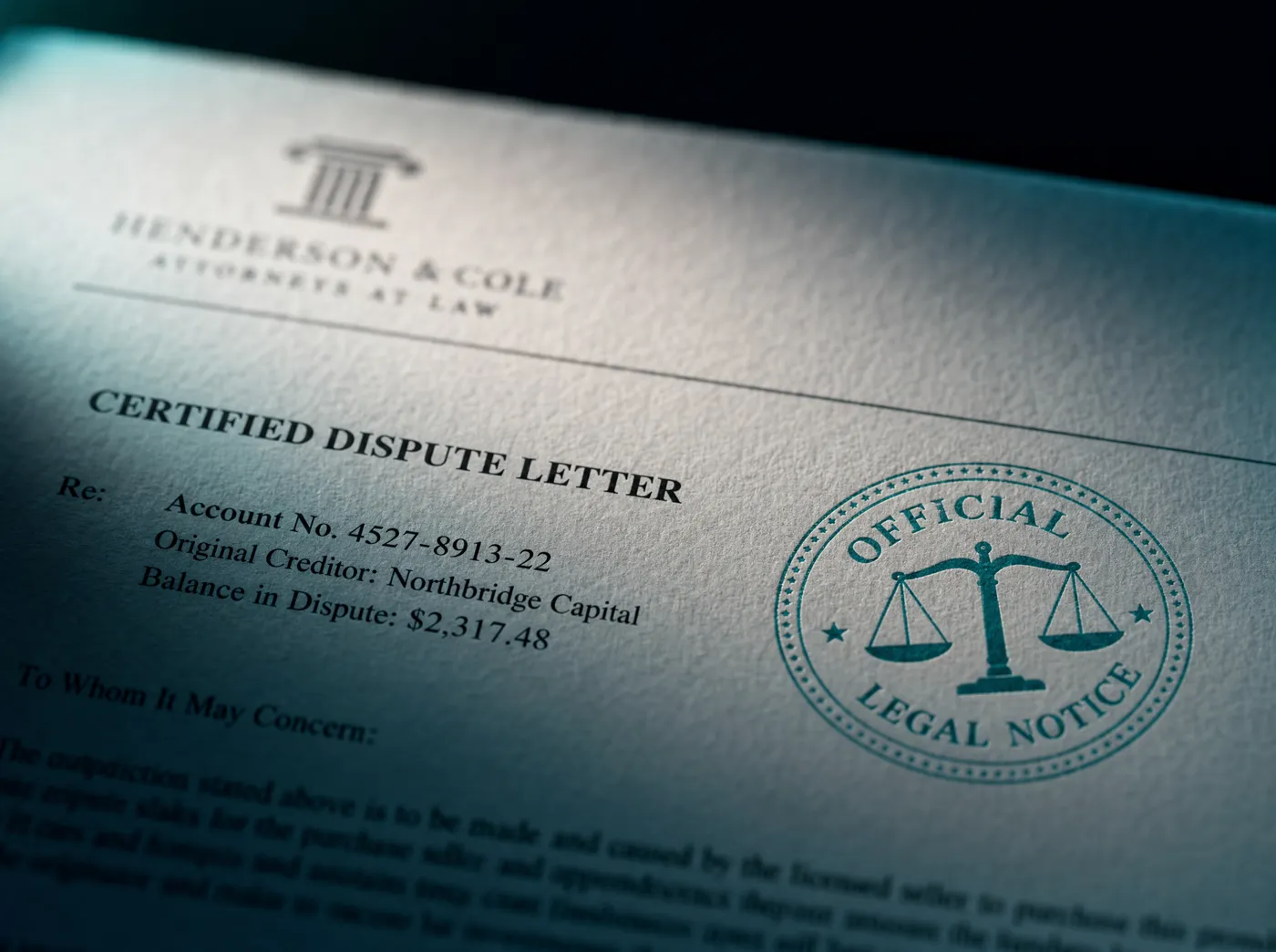

- Certified dispute letters that cite the exact statute

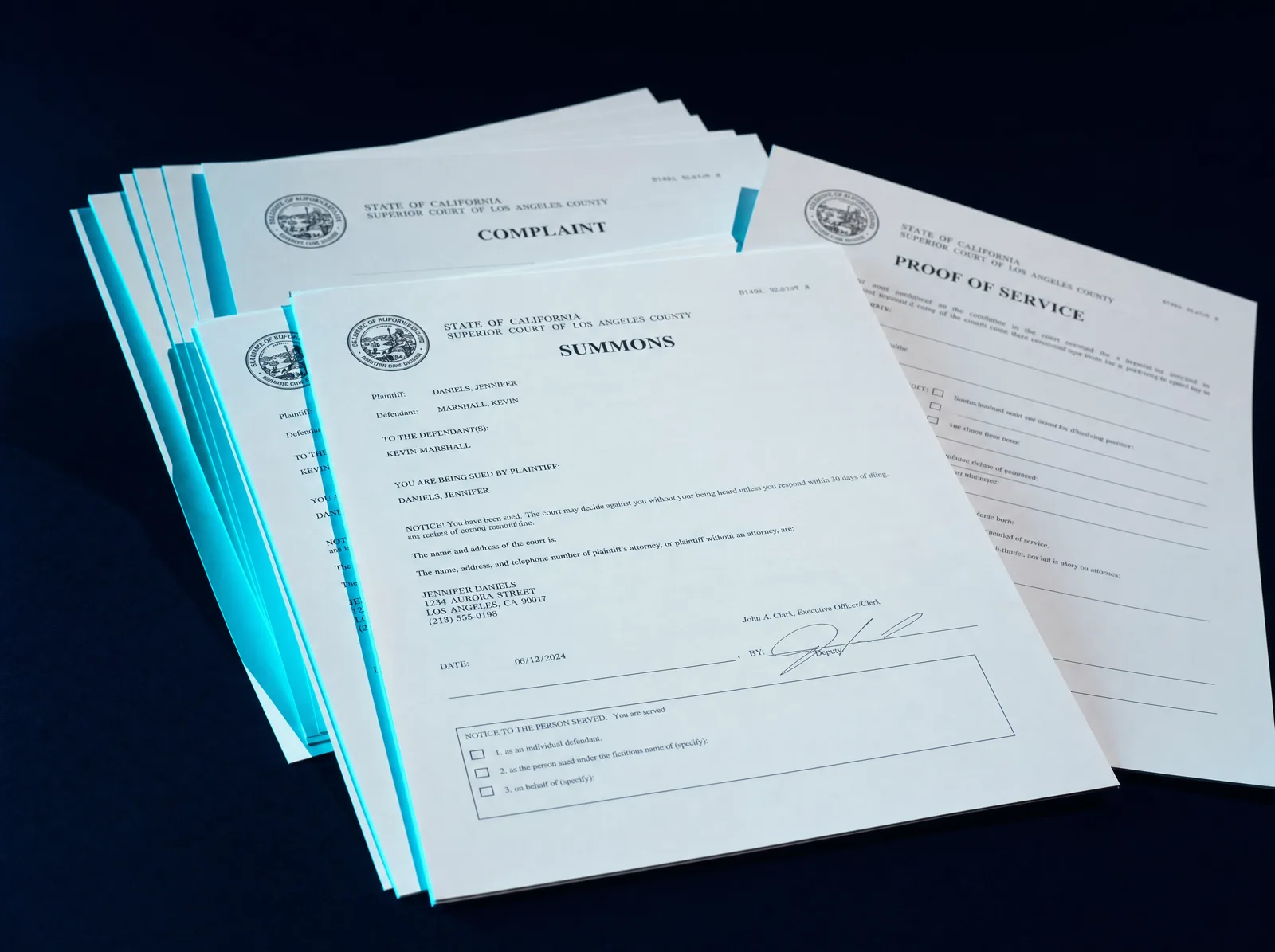

- Court-ready complaints, POS-010, CIV-100, JUD-100

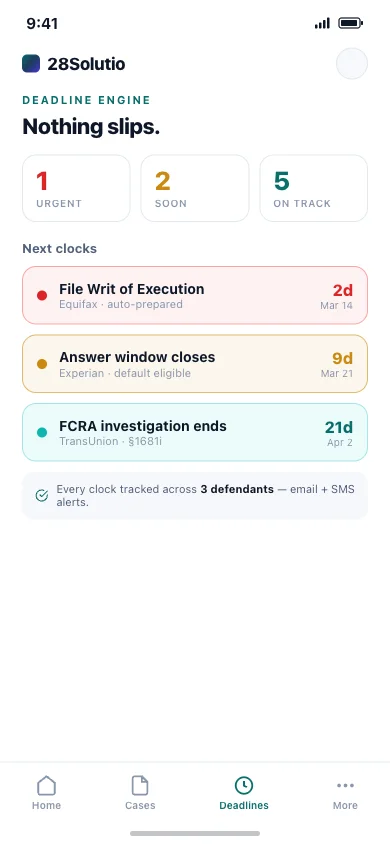

- Every FCRA / FDCPA deadline tracked across defendants

Every FCRA violation is worth $100–$1,000 in statutory damages (15 U.S.C. §1681n). Figures shown are illustrative.

What lands in your case file

The actual court paperwork —

generated for you.

Not a template to wrestle with. 28Solutio assembles the real, court-ready forms your county expects — filled from your case, ready to sign and file.

- Summons & Complaint — the suit itself, caption and all

- Proof of Service — so the answer clock starts clean

- Default-judgment packet when they don’t respond in time

The path to getting paid

CA & TX court-ready · 49 states + DC mappedFrom a disputed line to money in hand.

Four steps, one engine. The same system that drafts your first dispute letter prepares the writ that collects your judgment — court-ready in California & Texas today, expanding toward all 50 states + DC.

Step 1 · Dispute

Turn a bureau’s silence into a federal violation.

We prepare FCRA dispute letters that cite the statute by section — ready for you to mail certified to all three bureaus. When the bureau lets the 30-day clock run out, you’re left holding a documented violation and the evidence your case is built on.

statutory damages, per violation

Prepared for you

FCRA §1681Certified mail

The other situation

Wait — did a collector sue you?

Don’t ignore it — silence is how they win by default. Find your response deadline and make them prove the debt before the clock runs out. Straight answer: for California and Texas justice courts we now prepare your Answer — free with a free account; everywhere else, the free calculator plus your state’s own court form gets you filed on time. Just want the calls to stop? That’s the FDCPA validation letter — once it’s sent, the collector must pause collection until they prove the debt. We prepare it; you mail it.

Response-deadline estimator

I was sued — what do I do? →Pricing

Pricing, minus the maze.

Start with a letter. Win the whole case. Pick what fits right now.

The moat

Pro — win by default

$49/mo

$39 to start · cancel anytime

Unlimited disputes, plus your court-ready complaint and default-judgment packet — included, generated for you to file. When they don't answer, you keep 100% of the statutory damages.

See the litigation plan →Dispute letters

$35/dispute

pay-per-use · no subscription

Start here: AI writes it, we print it, and mail it USPS certified to all three bureaus. Your dashboard tracks delivery and the 30-day reinvestigation clock.

Start a dispute →Straight with you

No lawyer's name on the door.

Just the truth, on the record.

We'd rather lose your business than flatter you into a case you can't win. That's the whole difference — we show our work instead of asking you to trust a title.

If your case belongs with a lawyer, we tell you.

Strong, fee-shifting cases can cost you $0 with a consumer attorney — our triage says so and points you to free ones. We don’t hoard cases we shouldn’t take.

We tell you when you don’t have a case yet.

The intake grades your evidence honestly — if proving they received your dispute is the weak link, we say so instead of selling you a filing.

Not a law firm — you file it yourself.

We prepare the court-ready paperwork and track every deadline; you stay in control, and we say exactly that on every page. No hidden “representation.”

Results-or-refund, cancel anytime.

A defined money-back promise and no lock-in. You always see the price before you pay.

The law already wrote you a check. We help you cash it.

Upload your report. We find the violations, generate the letters, and build the lawsuit packet if they don't fix it. You file — we track every deadline.